Tokenization unlocks private credit

It's about how to get one of the world's largest lending markets on a more robust track.

JinseFinance

JinseFinance

This is a key distinction that most articles overlook.

Representative Tokenization: The blockchain serves solely as a transparent record system for off-chain lending. These tokens are non-transferable and non-tradable; the blockchain only provides operational upgrades (immutable ledger, real-time tracking). Figure primarily employs this model.

Figure's Data

Distributable Tokenization: Loans are natively issued and held on-chain as transferable tokens. Investors can hold, trade, and combine these tokens within the DeFi ecosystem. Platforms like Maple, Centrifuge, and Tradable are closer to this model.

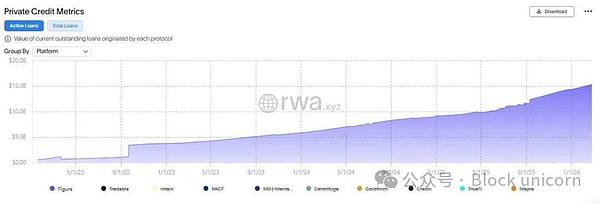

According to research data from HTX_Global, of the approximately $19 billion in active on-chain private lending, only about 12% is held in a transferable, distributable tokenized form. The remainder is "recorded but immovable." This is a crucial nuance in assessing the true state of the market. **Evolution Process** **Phase 0: Prehistory (2017-2019)** **2017: Centrifuge was founded as one of the first DeFi projects to integrate RWA. It initially focused on tokenizing invoices and accounts receivable through its Tinlake protocol (an open asset pool powered by smart contracts).** **2018: Figure was founded by Mike Cagney (former CEO of SoFi). The company focused on integrating blockchain into financial services, first launching Home Equity Credit (HELOC) based on blockchain infrastructure. Figure developed the Provenance Blockchain Foundation (a Layer 1 based on the Cosmos SDK) as its infrastructure.** 2019: Cadence (later renamed Percent) launched its first tokenized private debt product, attempting to reduce back-office costs by standardizing and reusing smart contract templates for structured products. Early challenges followed, such as higher-than-expected on-chain contract mirroring costs and insufficient demand for tokenized debt due to a lack of sufficient crypto-native investors to invest effectively. Phase 1: DeFi Integration and Early Development (2020-2021) 2020 (Centrifuge V1): Centrifuge proved that tokenized private credit could serve as collateral in DeFi, notably its integration with SkyEcosystem. Early 2021: Goldfinch launched, focusing on decentralized lending in emerging markets. This protocol enables cryptocurrency investors to provide loan funds to fintech institutions in developing countries (Indonesia, Mexico, Peru, Kenya). It employs a dual-pool model: retail funds enter a senior pool for stable returns (7-10% annualized), while community-elected junior supporters provide first-loss funding in exchange for higher returns. 2021: Maple launched as an institutional lending platform on Ethereum, using "pool representatives" for credit assessment. Initially serving institutional borrowers such as hedge funds, trading firms, and cryptocurrency market makers. TrueFi and Clearpool also entered the market. 2021: Figure began settling Home Equity Credits (HELOCs) on the Provenance Blockchain Foundation, reducing financing cycles from months to days and eliminating intermediaries. Mid-2021 to end of 2022: Active lending in the on-chain private lending market peaked at nearly $1.5 billion. Lending was primarily driven by cryptocurrency exchanges and market makers. Phase 2: Crypto Winter and Reset (2022) 2022: The crypto winter severely impacted on-chain private lending. Maple defaulted on $69.3 million in debt during institutional turmoil (the collapses of FTX/Alameda/3AC). Low-collateralized loans to crypto companies proved disastrous. Goldfinch experienced bad credit through its emerging market offerings. Total on-chain private lending value plummeted from its peak. Lending to crypto-native companies (trading desks, market makers) created a cyclical risk. The market began to shift towards real-world lending as a driver of recovery. Phase 3: Real-world Transformation and Institutional Investor Entry (2023-2024) 2023 (Centrifuge V2): Multi-chain expansion and institutional-grade fund structuring tools. New growth primarily came from real-world lending. 2023: Hamilton Lane tokenized its Senior Credit Opportunities (SCOPE) private credit fund on Ethereum and Polygon through Securitize, lowering the minimum investment from $5 million to $20,000. 2022 (Early): KKR launched its healthcare strategic growth fund on the Avalanche blockchain via Securitize. 2024: Hamilton Lane extended SCOPE to the Solana chain via the Libre platform. Mid-2024: Centrifuge had an outstanding loan balance of $289 million, primarily invested in consumer asset-backed securities (ABS), real estate bridge loans, and trade finance. Over 85% of loans issued through Centrifuge were financed via the Sky Protocol (formerly MakerDAO). 2024 (Centrifuge V3): Interoperability, Standardization, and Composability. Develop ERC-7540, an extension of ERC-4626, for standardizing asynchronous investing and redemption. End of 2024: BlackRock launches BUIDL (a tokenized money market fund), reaching $1.2 billion in assets under management within six months. Early 2024: The private lending tokenization space reaches approximately $8 billion, primarily driven by Figure, Centrifuge, Maple, Goldfinch, Clearpool, and Credix. Phase 4: Institutional Acceleration (2025) January 2025: Apollo launches the tokenized diversified credit fund (ACRED) across six blockchains via Securitize. By November 2025, its assets under management reached $170 million. In February 2025: Figure formed a joint venture with Sixth Street (Sixth Street committed $200 million in equity to Figure Connect for continued private lending liquidity). By mid-2025: Figure had tokenized over $13 billion in loans (primarily home equity lines of credit). It became the number one non-bank home equity line of credit lender in the U.S. It settled over $600 million in loans monthly on Provenance. September 2025: Figure listed on Nasdaq under the ticker symbol FIGR, raising $787.5 million in its IPO, valuing the company at $5.3 billion (later reaching $7.6 billion). October 2025: Total tokenized real-world assets (RWA) reached approximately $33 billion, with private lending accounting for $16-18 billion. As of November 2025: On-chain private lending exceeded $18.91 billion, with cumulative disbursements reaching $33.66 billion (RWA.xyz data). The value increased by 82% from the end of 2024, reaching $17.9 billion as of October 2025 (PwC data). Securitize issued nearly $4 billion in tokenized assets and is a tokenization partner of BlackRock, Apollo, Hamilton Lane, KKR, and VanEck. **Phase 5: Status Quo (Early 2026)** February 2026: Figure Technologies currently leads the market with approximately $15 billion in active loans, representing 75% of the total active loan volume of approximately $20 billion (RWA.xyz data). The total value of tokenized assets on the Provenance platform reached $1.2 billion in TVL. Hamilton Lane and Securitize launched an RWA-backed stablecoin on OKX's X Layer platform. This stablecoin is backed by tokenized exposure from Hamilton Lane's SCOPE fund and employs a dual-token architecture to separate yields from the stablecoin itself. The tokenized private lending market continues to expand into the DeFi composability space: Apollo's ACRED fund is being used in leveraged cycles on platforms like Morpho and Kamino, demonstrating that on-chain assets can be combined in ways that are impossible in traditional finance. Industry expectations for 2026 include major institutions "transitioning from pilot phases to large-scale, production-ready products," and the potential for on-chain lending to receive ratings from traditional rating agencies. How Tokenized Private Lending Works** **Token Standards and Structure** **Loan-Specific Tokens:** Each loan is tokenized into one or more ERC-20 tokens, representing a claim to the cash flow of that asset. For example, real estate lenders issue tokens that entitle holders to mortgage repayments. These tokens typically constitute securities and must be issued under exemptions (Reg D for accredited investors, and Reg A+ for broader but restricted retail investors).** **Loan Pool Model:** Lenders contribute to a public pool of funds, which then distributes loans to borrowers on their behalf. Loans are represented on-chain as debt securities (non-tradable tokens) linked to NFTs, while lenders receive ERC-20 tokens representing their share of the pool. Smart contract enforcement clauses mean that if a borrower fails to repay the loan, the loan defaults, triggering pre-defined remedies. Fund tokenization: The fund structure itself is tokenized (e.g., Hamilton Lane's SCOPE). Investors hold tokens representing fund units, rather than direct claims on individual loans. This is currently the mainstream institutional model. Key Standards: ERC-20: Standard fungible token for loan pool shares and fund tokens. ERC-721 (NFT): For individual loan representations in certain protocols. ERC-4626: Standard for tokenized vaults for yield positions. ERC-7540: An extension of ERC-4626 for asynchronous investing and redemption, a leading DeFi RWA standard developed by Centrifuge. Tiered Structure: Advanced/Junior Tiered Structure (Centrifuge's DROP/TIN model) allows for risk-return differentiation. Lifecycle Management. Smart Contract Processing: Loan Issuance and Interest Accumulation; Token Holder Collection and Distribution; Redemption and Principal Return; Compliance Checks (Whitelist, KYC/AML, Jurisdiction Restrictions); Default Trigger Mechanism and Waterfall Repayment Mechanism; Transparency Issues. This section of the article applies the RWA Transparency Framework, which distinguishes between the actual allocated content and the content merely presented on-chain. What does Figure's dominance really mean? Figure accounts for approximately 75% of tokenized private lending. However, Provenance is a specially constructed chain whose smart contracts require governance approval. As Glider co-founder Brian Huang points out: "Unless the asset is composable, on-chain assets are no more useful than off-chain assets. Provenance is not composable." This means that, in dollar terms, the vast majority of tokenized private lending is essentially an operational upgrade, rather than a distributable, DeFi-composable asset. These loans are not tradable tokens that investors can freely transfer, combine, or use across ecosystems. This is crucial for transparency analysis. The 12% Problem: According to HTX research, only about 12% of on-chain private credit is held in a transferable tokenized form. The rest, while documented, cannot be distributed. While some say tokenized private credit is worth $20 billion, a more accurate figure for truly distributable, composable tokenized credit should be between $2 billion and $3 billion. On-Chain Verifiable Content: Fully verifiable: Token ownership, transfer history, fund share balance, smart contract terms, compliance status (whitelist), and payment and distribution. Partially verifiable: Total outstanding loan value (depending on oracle/report accuracy), collateral ratio (for overcollateralized models). On-chain verifiability includes: borrower creditworthiness, actual loan performance (still relying on off-chain reports), collateral quality of off-chain assets, true default rate, and recovery rate. Underlying credit risk assessment, underwriting, and counterparty evaluation remain entirely off-chain. Blockchain provides transparency at the token layer, but not necessarily at the asset layer.It's about how to get one of the world's largest lending markets on a more robust track.

JinseFinanceThe future may not belong to any particular form of currency, just as it never has. It may belong to the range from cash to digital currency.

JinseFinanceCryptocurrency, Token Economy, Tokenization of Equity in Non-Listed Companies: A Trillion-Dollar "Siege" and Attention Stealed by Perpetual Contracts. Golden Finance: How can equity tokenization break down the institutional monopoly on equity in non-listed companies?

JinseFinanceGold, which has been dormant for thousands of years, is the eternal belief of mankind. When war, unrest or inflation occurs, gold is the last refuge of value.

JinseFinanceProjects like Ventuals, Zoshi, and FreeStock are exploring different paths to tokenizing private equity.

JinseFinanceDaniel Maeda announced Brazil's CVM's plan for a 2024 regulatory sandbox during Rio Innovation Week, emphasising tokenisation and market evolution.

Bitcoinworld

BitcoinworldCredit Suisse and the Swiss Football Association are launching an NFT collection to support women’s football. The Ethereum-based NFT collection consists of 756 digital art portraits of Swiss women’s national team players.

TheBlock

TheBlockThe bank concluded a half billion dollar settlement with U.S. prosecutors on Monday.

Beincrypto

BeincryptoOne of the world’s biggest banks insists it is in a “strong” financial position, amid fears of a looming Lehman Brothers moment that could spark a major crisis.

Others

OthersThe crypto bear market had largely been brought about by the crash of various lending platforms. Crypto lending firms such ...

Bitcoinist

Bitcoinist