After we put the money into Huma Finance Arf Pool, these assets will be stored by Arf in a bankruptcy-isolated SPV (special purpose entity, a legal entity created for a specific or temporary purpose, mainly for risk isolation).

After we put the money into Huma Finance Arf Pool, these assets will be stored by Arf in a bankruptcy-isolated SPV (special purpose entity, a legal entity created for a specific or temporary purpose, mainly for risk isolation).

As a service provider, Arf Financial GmbH provides services to SPV. Lending, cross-border payments, transaction settlement and risk management are carried out here. After a transaction is completed, SPV will return the money and profits in the Pool to the chain. Arf Financial GmbH has no control over the corresponding Pool funds.

6/ Fill in the gaps

Here are two additional points:

1. Circle's official website has a very detailed introduction to Arf:https://www.circle.com/en/case-studies/arf

Arf does a good job in risk control, but this also leads to some problems, such as the need for KYC before depositing, which is not friendly to many DeFi players. And, I personally think that Huma Finance's UI/UX still has room for improvement.

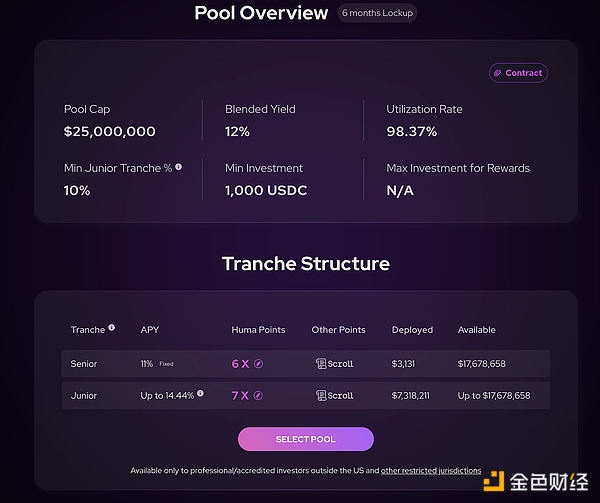

2. Cooperation with Scroll

Currently, we can deposit USDC into Huma on Scroll, and achieve three benefits from one fish - 10% + financial management income + Huma points + Scroll points.

7/ Finally

Why have I been looking at this kind of financial products recently? Because after I cleared my position some time ago, most of my assets were U, so I wanted to find a good place for these U to manage their wealth.

From my personal point of view, before the market shows a potential upward trend, I will not be fully invested or leveraged, and at most do some short-term swing operations.

On the product side, v2 implements a more complex product structure, such as the addition of Senior, which we will mention below. Tranche, Junior Tranche, and First Loss Cover. Simply put, this upgrade is a subdivision of the functions to meet the needs of users with different needs.

On the product side, v2 implements a more complex product structure, such as the addition of Senior, which we will mention below. Tranche, Junior Tranche, and First Loss Cover. Simply put, this upgrade is a subdivision of the functions to meet the needs of users with different needs.  JinseFinance

JinseFinance